Consignment Inventory Accounting Defined + Journal Entries %%page%%

Consignment inventory is common in industries where companies transfer their goods to the dealer, which distribute or sell them further. The dealer, in this case, is only responsible for its distribution or retail operations. The consignee now provides a summary to the consignor of all transactions it has made relating to the consignment.

Products

Taking inventory on consignment allows you to offer your customers a larger variety of goods with significantly lower financial risk since you aren’t paying for the inventory until it is sold. To completely understand consignment accounting entries, it is vital to understand the common terms used in this domain of work. The consignee also has the option to return any unsold or damaged goods to the consigner. Other names used for consignment inventory are consignment goods or consignment sales.

How to Calculate Inventory Turnover Ratio? (Definition, Using, Formula, and Example)

He has been the CFO or controller of both small and medium sized companies and has run small businesses of his own. He has been a manager and an auditor with Deloitte, a big 4 accountancy firm, and holds a degree from Loughborough University. The selling and commission expenses relate only to goods which have been sold and can be taken direct to the appropriate expense account. Imagine that Susan, a jewelry designer, decides to consign a selection of her handcrafted necklaces to “Glamour Boutique,” a local fashion store.

- He has been a manager and an auditor with Deloitte, a big 4 accountancy firm, and holds a degree from Loughborough University.

- The consignor continues to own the goods until they are sold, so the goods appear as inventory in the accounting records of the consignor, not the consignee.

- It is entitled to a commission of 12% including the del-credere commission.

- People sell toys, furniture, shoes, and clothes on consignment frequently.

- As part of consignment inventory management, both parties should practice proper accounting of consigned goods.

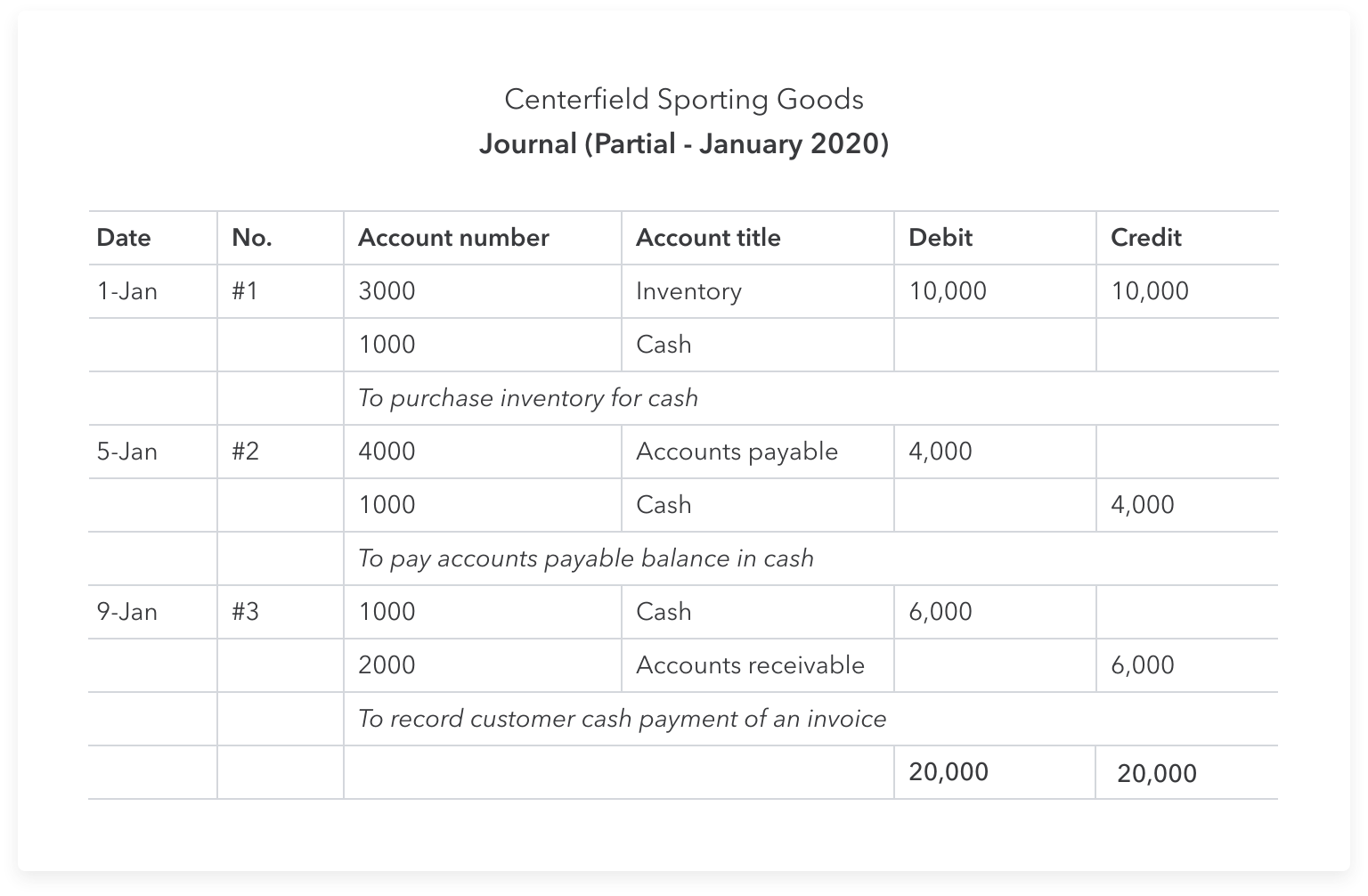

Accounting Entries in books of Consignee

However, some consignors may use the following double entry to transfer inventory into a different account, for the organization. As mentioned, there are usually two parties involved in the can i deduct back taxes paid consignment deal. The first party, the consignor, is the company that provides the goods. The other party, the consignee, is the company or business that holds the physical inventory.

Account Sale is a statement showing the details of goods received, goods sold, expenses incurred, the commission charged, remittances made, and due balance. It is remitted by the consignee to the consignor of goods periodically. Consignment accounting balance signifies profit or loss upon consignment and is moved to the "Profit & Loss section in Consignment Account." As a result, the consignment profile is closed. Profits or losses on consignment is another type of nominal accounting. When there are several consignments, the total amount of all consignment assets is sent to this account. After the calendar year, the profit or loss on consignment accounts is ended by moving its amount to the General Profit & Loss Account.

When providing items to the consignor, a consignee submits the proforma invoice for details of products sold, plus the consignee sends record sale data. A separate account for consignment accounting is kept for the settlement and balancing of records. The consignment inventory accounting journal represents the transfer of inventory from the normal inventory account to a separate consignment inventory account. The inventory is still the property of the consignor, and no entry is made by the consignee. This journal entry indicates the transfer of inventory from the standard inventory account to a separate consignment inventory account.

If the consignee is unable to sell all goods, they are able to return the goods to the consignor (before a specified date). Therefore, the consignor bears the risks and rewards of ownership, while the consignee is not required to pay for the goods until they are sold. He does not make an accounting entry when he receives the goods consigned to him. He may however, keep the record of goods received in a separate book known as consignment inward book. Yes, because both parties must keep track of consignment transactions. For the consignee, proper accounting ensures that consigned goods aren’t mixed with other goods.

On the other hand, if the consignee fails to sell all the goods transferred, they will return those goods to the consignor. In that case, the consignor doesn’t need to pass any double entry since the risks and rewards stay the same. The first double entry is to record the sale made through the consignee, while the second double entry is to record the decrease in inventory. Therefore, the consignor can only reduce its inventory account once it receives the sale proceeds. With consignment inventory, the consignor transfers the goods to the consignee, which sells the goods to customers. Once the consignee sells the goods, the risk and rewards related to the inventory get transferred.

As with any other sale transaction, it consists of two double entries to the accounts. The consignor records the inventory on consignment because they still own the consigned goods until sold to final customers. The consignee does not show consigned inventory on their balance sheet. Try Unleashed for free today or book a demo to learn how we can help your business make light work of consignment inventory accounting and stock management.

They would also purge the related amount of inventory as a debit to cost of goods sold and a credit to inventory. As the expenses relate to the consignment and are a cost of bringing the inventory to its present location and condition, they are debited to the consignment inventory account. The credit entry as usual is either to accounts payable or cash depending on the terms agreed with the supplier. Consignment accounting refers to the accounting methods and practices used to record and report transactions related to consignment arrangements between a consignor and a consignee. When the consignor receives the Account Sales Report from the consignee, the consignor then completes the consignment accounting.